The renewable energy sector continues to expand, despite policy uncertainty under the Trump administration.

Nebraska Solar Incentives: 2025 Overview

Nebraska provides incentives to make solar energy more accessible. Homeowners can benefit from the 30% Residential Clean Energy Credit, reducing installation costs, and some Nebraska utilities offer net metering, allowing residents to earn credits for excess energy to offset future bills. With Nebraska’s sunny climate and these financial benefits, going solar is a practical way…

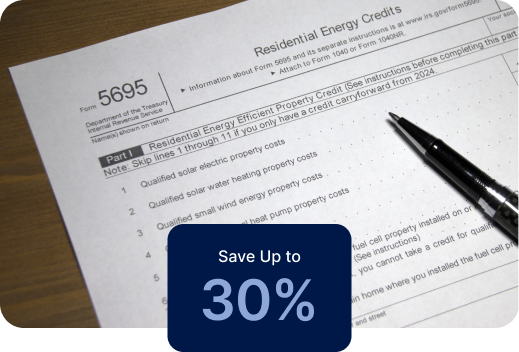

Residential Clean Energy Credit

The Clean Electricity Investment Credit (previously called the Federal Investment Tax Credit) helps lower the cost of installing solar panels by 30%. This credit covers everything: the solar panels, equipment, labor, permits, and even sales tax.

For example, as of 2025 the average cost of a 10 kW solar system in the U.S. typically ranges between $21,000 and $29,500 before applying any federal tax incentives. After claiming the 30% Clean Electricity Investment Credit, the price drops to around $14,980 to $21,070, depending on the state and other factors like equipment quality and labor costs.

To claim this credit, you must buy your solar system with cash or a loan (leases don’t qualify). You also need to owe enough in taxes to claim the credit, but if you don’t, you can carry it over to future years until 2034.

Claiming the Clean Electricity Investment Credit is simple!

Step 1

Print IRS Form 3468

Step 2

Fill out the form using info from your installer

Step 3

Submit it when you file your taxes

What are the top solar incentives in Nebraska?

Besides the Clean Electricity Investment Credit (former ITC), homeowners can take advantage of several outstanding incentives that significantly enhance the return on investment for solar panels. Here are some of the most effective ways to lower your solar installation costs.

Incentive

Savings

Summary

Residential Renewable Energy Tax Credit

A taxpayer may claim a credit of 30% of qualified expenditures, after deducting incentives, with no upper limit for a system that serves a dwelling unit located in the United States that is owned and used as a residence by the taxpayer. Expenditures with respect to the equipment are treated as made when the installation is completed. If the installation is at a new home, the “placed in service” date is the date of occupancy by the homeowner. Expenditures include labor costs for on-site preparation, assembly or original system installation, and for piping or wiring to interconnect a system to the home. If the federal tax credit exceeds tax liability, the excess amount may be carried forward to the succeeding taxable year. The excess credit may be carried forward until 2019, but it is unclear whether the unused tax credit can be carried forward after then.

Residential Renewable Energy Tax Credit

A taxpayer may claim a credit of 26% of qualified expenditures, after deducting incentives, with no upper limit for a system that serves a dwelling unit located in the United States that is owned and used as a residence by the taxpayer. Expenditures with respect to the equipment are treated as made when the installation is completed. If the installation is at a new home, the “placed in service” date is the date of occupancy by the homeowner. Expenditures include labor costs for on-site preparation, assembly or original system installation, and for piping or wiring to interconnect a system to the home. If the federal tax credit exceeds tax liability, the excess amount may be carried forward to the succeeding taxable year. The excess credit may be carried forward until 2019, but it is unclear whether the unused tax credit can be carried forward after then.

Residential Renewable Energy Tax Credit

A taxpayer may claim a credit of 22% of qualified expenditures, after deducting incentives, with no upper limit for a system that serves a dwelling unit located in the United States that is owned and used as a residence by the taxpayer. Expenditures with respect to the equipment are treated as made when the installation is completed. If the installation is at a new home, the “placed in service” date is the date of occupancy by the homeowner. Expenditures include labor costs for on-site preparation, assembly or original system installation, and for piping or wiring to interconnect a system to the home. If the federal tax credit exceeds tax liability, the excess amount may be carried forward to the succeeding taxable year. The excess credit may be carried forward until 2021, but it is unclear whether the unused tax credit can be carried forward after then.

Residential Renewable Energy Tax Credit

A taxpayer may claim a credit of 30% for the installation which was between 2022-2032 (Systems installed on or before December 31, 2019 were also eligible for a 30% tax credit), with no upper limit for a system that serves a dwelling unit located in the United States that is owned and used as a residence by the taxpayer. Expenditures with respect to the equipment are treated as made when the installation is completed. If the installation is at a new home, the placed in service date is the date of occupancy by the homeowner. Expenditures include labor costs for on-site preparation, assembly or original system installation, and for piping or wiring to interconnect a system to the home.

Solar Rebate Program

Customers who install a qualifying solar system through a Solar/Customer-Owned Generation Trade Ally qualify for a one-time $2,000 solar rebate from OPPD.

Residential Solar Renewable Energy Rebate

Lincoln Electric System will make a one-time capacity payment to the owner of the renewable generation based on the contribution of peak reduction by the renewable resource, valued at a traditional resource cost of $1,000 per kW-AC. Capacity increases or additions in future years will be eligible for the capacity payment. The total amount customers can receive is determined by the type and efficiency of the technology installed.

Residential Solar Renewable Energy Rebate

Lincoln Electric System will make a one-time capacity payment to the owner of the renewable generation based on the contribution of peak reduction by the renewable resource, valued at a traditional resource cost of $1,000 per kW-AC. Capacity increases or additions in future years will be eligible for the capacity payment. The total amount customers can receive is determined by the type and efficiency of the technology installed.

Disclaimer: The information provided here regarding solar incentives, tax credits, and rebates is for general informational purposes only and may vary based on your specific circumstances. For exact details, eligibility requirements, and current rates, we recommend consulting a certified solar installer or a tax professional. Incentives can differ by location, utility provider, and individual project, so it’s important to get personalized advice for your solar installation. Always verify the most up-to-date information from your local solar installer to understand how these incentives apply to your project.

Knowledge Base

Find everything you need to know about solar in your state and nationwide

EPA Restores $7 Billion ‘Solar for All’ Grants After Temporary Freeze

The EPA has reinstated the $7 billion Solar for All grant program, allowing funds to support low-income and disadvantaged communities in accessing…

Rising electricity prices: the cost of repealing clean energy incentives

Homeowners and businesses could see electricity bills surge as Congress debates cutting clean energy tax credits that have helped keep energy costs…

Time running out: Clean Energy Tax Credits at risk as Congress debates repeal

Millions of Americans can still benefit from federal clean energy tax credits – but a proposed bill could put these savings at…

Community solar expands by a record 1.7 GW in 2024, surging 35%

The U.S. community solar market experienced its strongest year yet in 2024, adding 1.7 GW of new capacity – an increase of…

Illinois moves to streamline residential solar permitting with new legislation

A proposed bill in Illinois aims to simplify solar permitting through automation, reducing delays and costs for homeowners while accelerating the adoption…

Get a Quote

Discover the Ideal Solar System for Your Home in Just a Few Clicks!